The year 2022 was the year favouring the Indian Banking sector as their stock prices were at an all-time high. Banks are the important entities required for the survival of the economy, as it inculcates the habit of savings among various individuals, these savings are then mobilized by the bank in the form of deposits, and the same are given as credit to the people who are in need of money. For an investor before purchasing Yes bank shares, it’s important to know the Yes Bank fundamentals which will help the investor to predict future performances.

Yes Bank is considered one of the major private banks, founded by Rana Kapoor and the late Ashok Kapoor, and is engaged in providing various banking services to its customers. It operates in Retail, MSME and corporate banking sectors. It provides a wide range of services to both retail and corporate customers in the form of retail banking and asset management services. It is presently the 7th largest private sector bank with a market capitalization of 49000 crores.

Yes Bank is regarded as one of the new generation private banks which was allowed to start its banking operations by RBI in the post liberalization era. It was founded by Rana Kapoor and the Late Ashok Kapoor in 2004.

The bank was involved in unscrupulous banking practices as it provided loans to those parties or business entities who were not able to raise funds from anywhere.

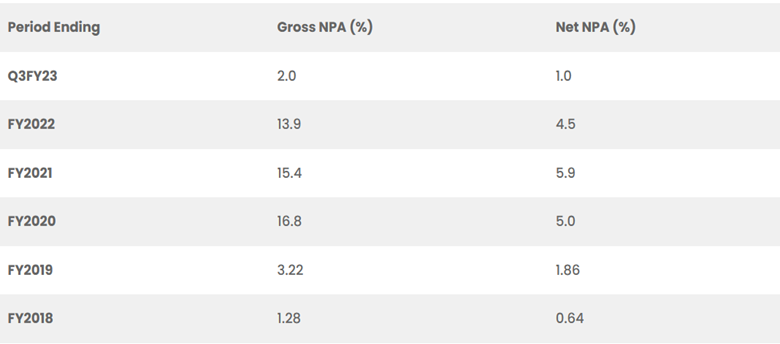

Finally, these unscrupulous practices were highlighted in the public in late 2019. As the NPAs of the bank had increased exponentially.

Yes Bank Crisis

In the last quarter of 2019, the bank’s gross NPAs( Non- Performing Assets) increased exponentially from 7.4% in the previous quarter to 18.4% in Dec 2019. Which resulted in a huge loss of around Rs.18,564 crores as compared to Rs 1001 crores profit in the same quarter in 2018.

RBI came up as the saviour of the Yes Bank in 2020, as they cannot let such a large bank turn down its business which has the huge public interest at stake.

So, in March RBI took the first step and put a moratorium on Yes Bank for 30 days. This means the bank won’t be allowed to provide large withdrawals, provide/renew loans, make investments, borrow money, etc.

Moreover, in order to uplift the bank from the liquidity crisis, several large banks were roped in by RBI i.e. SBI, HDFC bank, ICICI Bank, and Axis Bank. Various banks invested money in the bank for lock-in period of 3 years by taking 75% of its stake, SBI solely bought about 48% stake for 6,050 Crores.

RBI appointed Prashant Kumar who was the Chief Financial officer and Deputy managing director at the State bank of India as an administrator in the Yes Bank.

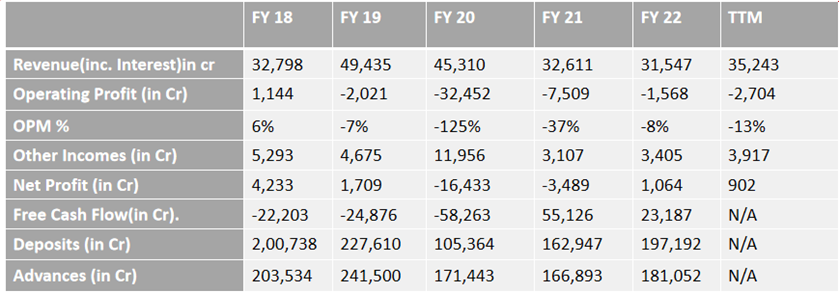

If we look at the topline of the stock, then it has obtained minimal growth in its revenue after the pandemic. The recovery was not that aggressive after the pandemic

As of now, Yes Bank is incurring losses in its operations, that’s why the Operating profit is negative in various financial years consecutively.

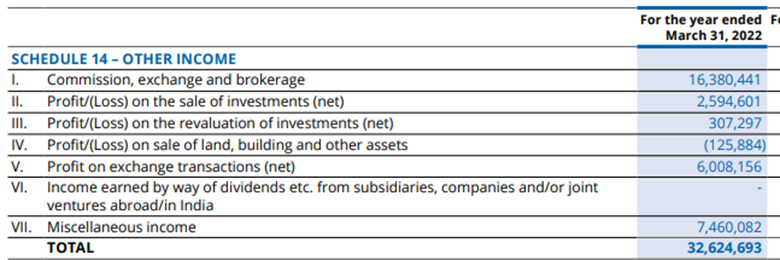

The only saviour which kept the net profit of the company positive is the income generated from other sources such as commission, exchange and brokerage, profit from the sale of investments etc.

Source: Annual Report

The deposits and advances are the two major segments required for the Bank to increase its profitability and goodwill. Yes Bank has shown significant growth both in its deposits and advances in the post crisis period.

If we look at the free cash flow, even though the bank is able to generate minimal profit through the financial year, free cash flow has shown a sharp rise from -58,263cr in FY20 to 55,126cr in FY21. This is because the company has written off its Non-performing advances, which led to a sudden fictitious rise in Company’s free cash flow. This also has led to decline in Bank’s non-performing assets(NPAs).

Source: TradeBrains

Ratio Analysis

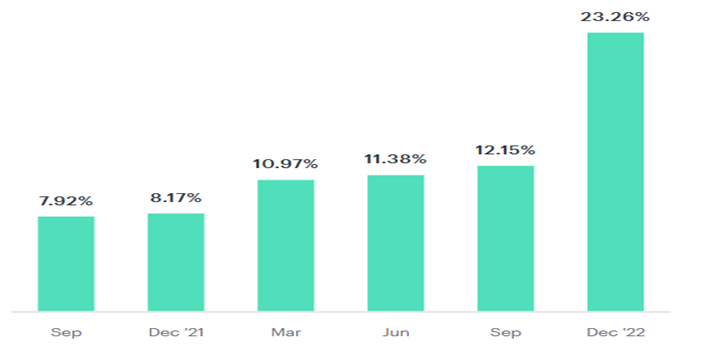

Recent fresh positions made by the FIIs( Foreign Institutional Investors) have improved both ROE and ROA of the stock substantially.

As it’s visible in the graph, the FIIs have almost doubled their investments in the stock.

FIIs Data Source: Tickertape

There is a minimal rise in the CASA ratio of the bank if compared to the post-crisis period, but it is still on the lower side if we assess the whole performance of the stock throughout the financial years.

There is sharp increase in the valuation ratio(P/E) of the bank might be due to an increase in substantial holdings of the FIIs. On the contrary, P/B ratio remains stable.

Peer Comparison

Yes Bank Peer Comparison

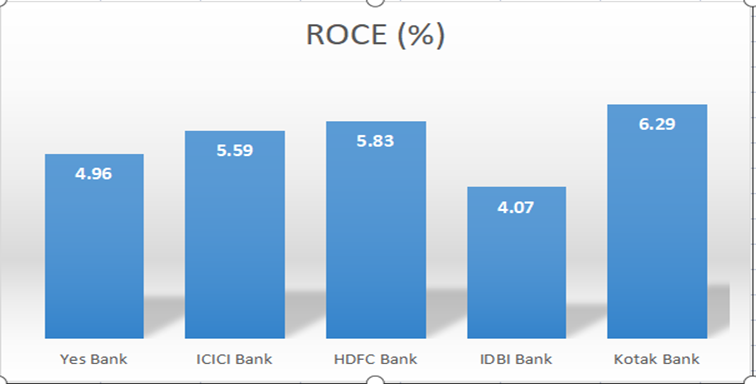

Yes bank has provided better ROCE(Return on Capital Employed) than most of its rivals i.e ICICI Bank and IDBI bank.

Yes bank valuation ratio or P/E ratio is higher than its competitors.

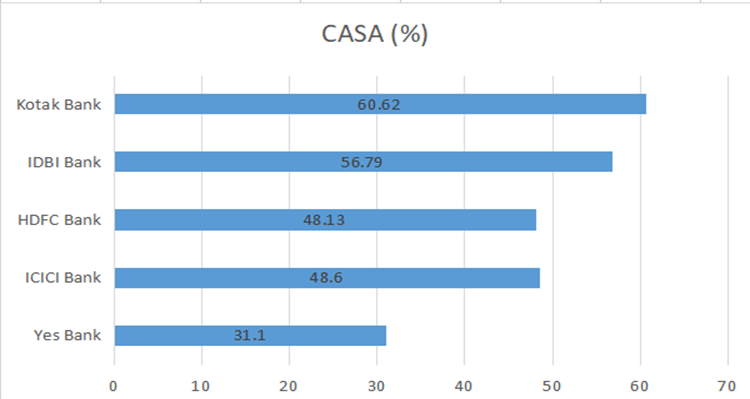

If we compare the CASA ratio, the competitors of Yes Bank have far better CASA ratio than Yes bank itself.

CASA

Future Prospects and Risks

After the core financial analysis of the company now let us look at its future potential and sources of risk

Prospects

With FIIs doubling their investments recently in Dec 2022 have raised the potential of the company towards the aspect of increasing their market share.

Recently, Yes Bank has partnered with Falcon, which will provide him access to various financial services and it will be ultimately offered to the bank’s customers.

Since the Bank would remain in its reconstruction phase for another few years. Therefore, the bank’s finance margin is less likely to improve.

After Bombay high court denial to write off AT-1 Bonds. Both Yes Bank and RBI have filed petitions in the Supreme Court. These AT-1 bonds have created a contingent liability of 8.4k Crore on the bank.

Yes Bank has a far lower CASA ratio than its rivals which makes experts hesitant about the stock.

Expiry of the lock-in investment period which was initiated by RBI as part of the bank’s reconstruction phase in 2020.

Conclusion

Though the bank has shown large improvements in FY22 as compared to other financial years in the post crisis period. It still has a long way to go as its rivals are also stressing hard to increase their profitability in the business. Therefore, in the coming years Yes Bank would face stiff competition from its rivals in every aspect. It’s time for the bank to recover quickly and regain its lost market share.